For years, brands could say a lot and prove a little. The Corporate Sustainability Reporting Directive (CSRD) flips that script with standardized data, comparable metrics, and independent assurance. In practice, this is Europe’s most effective CSRD greenwashing shield: if a claim can’t be proven, it won’t pass audit—internally or publicly.

Who is this for? SME leaders, sustainability teams, CFOs, and students who need a clear, practical guide to CSRD compliance, ESRS standards, and what to do now to avoid unintentional greenwashing.

How CSRD helps prevent greenwashing

CSRD closes the “marketing loophole” by requiring consistent, auditable disclosures aligned to European Sustainability Reporting Standards compliance. It mandates governance over sustainability data like financials, introduces external assurance, and ties climate targets to the EU Taxonomy CSRD framework, cutting room for vague or irrelevant claims.

- Standardization: comparable KPIs across companies and sectors.

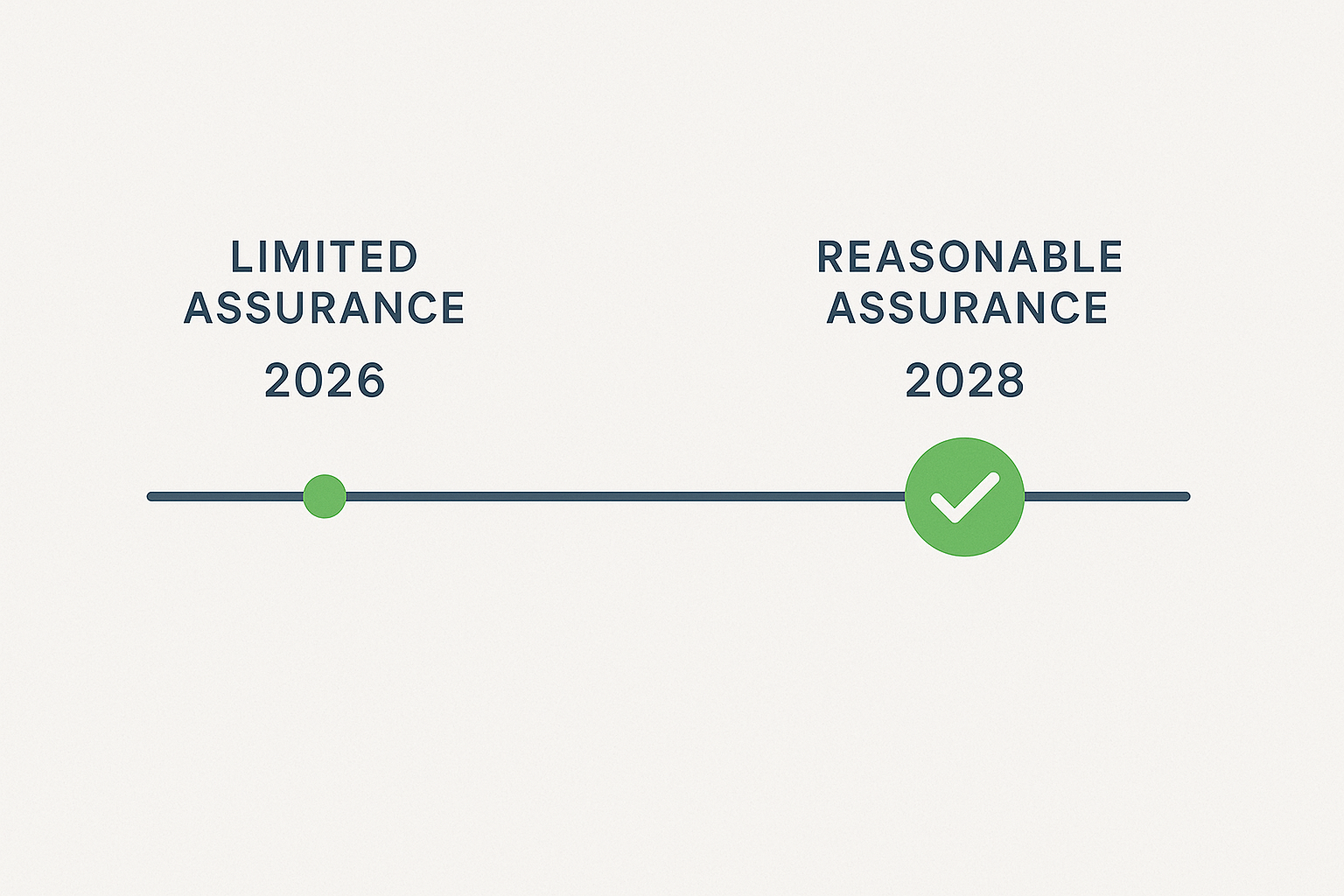

- Auditability: control environments, evidence trails, and limited → reasonable assurance.

- Scope discipline: boundary clarity reduces cherry-picking and selective disclosure.

Double materiality: two lenses that kill selective storytelling

Under CSRD, materiality works both ways: your company’s footprint on people and planet and how sustainability issues affect performance and risk. That dual lens is the enemy of one-sided narratives and a cornerstone of sustainability reporting transparency.

Tip: Run workshops with finance, risk, and ops. Co-own your double materiality assessment to prevent siloed claims.

ESRS: the language of credible sustainability data

ESRS sets out topic-specific requirements (E, S, and G) so disclosures are consistent, comparable, and evidence-based. This is where CSRD sustainability claims substantiation becomes operational—what to collect, where to publish, and how to document controls.

EU Taxonomy: one dictionary, fewer excuses

The EU Taxonomy CSRD link provides consistent definitions of what qualifies as sustainable. Fewer euphemisms, more comparable numbers. That reduces subjective interpretation—the gray area where CSRD anti-greenwashing wins are made.

External assurance: sustainability data gets audited like financials

Third-party scrutiny is a powerful anti-greenwashing tool. CSRD introduces CSRD external assurance requirements so that sustainability KPIs face the same skepticism and testing as your income statement.

CSRD software: features that prevent unintentional greenwashing

- Double materiality modules and stakeholder mapping.

- Data validation & audit trails for CSRD data verification process.

- ESRS-aligned templates, gap analysis, and CSRD software platforms 2025 integrations.

- Versioning, approvals, and evidence repositories for assurance review.

Value chain transparency (scope matters)

CSRD requires reporting across the value chain—not just your HQ. That expectation of upstream and downstream visibility is how CSRD value chain transparency stops selective disclosure and product-page green gloss.

Penalties & liability: what happens if you get it wrong

CSRD sits alongside consumer-protection and securities laws. As member states harmonize enforcement, expect tougher responses to misleading sustainability disclosures, including potential CSRD criminal enforcement penalties in some jurisdictions. The safe path is strong controls and early assurance.

CSRD vs NFRD: what changed (and why it matters for greenwashing)

| Topic | NFRD (old) | CSRD (current) | Anti-greenwashing impact |

|---|---|---|---|

| Scope | Large public-interest entities | Much wider set of companies incl. listed SMEs (with phase-ins) | Reduces “reporting gaps” across competitors |

| Standards | Looser frameworks | ESRS standards with detailed quantitative disclosures | Less ambiguity; comparable metrics |

| Assurance | Often none | CSRD mandatory audit (limited → reasonable) | Independent testing of claims and data |

| Materiality | Financial materiality focus | Double materiality assessment | Stops one-sided stories |

| Taxonomy link | Emerging | EU Taxonomy CSRD alignment | Common definitions reduce spin |

| Controls | Limited guidance | Governance, policies, and due-diligence expectations | Stronger systems = fewer errors |

Deep dive: CSRD vs NFRD greenwashing explainer.

CSRD timeline & assurance milestones

| Period | What to do | Why it matters for greenwashing |

|---|---|---|

| Now → 2025 | Run CSRD gap analysis tools, map data owners, set evidence repositories | Prevents last-minute errors and overclaims |

| By 2026 | Meet CSRD external assurance requirements (limited assurance) | External testing of methodologies and controls |

| 2026–2027 | Harden controls, extend value-chain coverage, refine CSRD transition plan requirements | Closes data gaps; improves comparability |

| By 2028 | Target reasonable assurance readiness; align with science-based targets CSRD | Green claims must stand up to deeper scrutiny |

See also: CSRD reporting obligations timeline.

How to avoid unintentional greenwashing in CSRD reports

1) Scope claims precisely

Define boundaries and functional units. If a claim applies only to packaging or a pilot site—say so.

2) Base claims on ESRS + Taxonomy

Anchor numbers in ESRS standards and EU Taxonomy CSRD criteria to cut subjectivity.

3) Build an evidence trail

Keep datasets, assumptions, and calculations in an auditable repository for assurance reviewers.

4) Use independent reviewers

Engage verifiers early for material topics—this is central to CSRD anti-greenwashing.

5) Publish method summaries

Plain-language pages linked from claims: boundaries, baselines, uncertainty, and trade-offs.

6) Treat “neutral” with caution

Avoid “carbon neutral” language without robust reduction pathways and clearly disclosed residuals.

Toolkit: How to avoid greenwashing CSRD report • CSRD data verification process

CSRD vs the (paused) Green Claims Directive

Think of CSRD as the corporate reporting backbone and the proposed Green Claims Directive as product-claim guardrails. While the latter is paused, CSRD continues—requiring robust disclosures that indirectly police marketing statements. See: CSRD greenwashing shield.

Transition plans that pass the sniff test

CSRD expects credible, time-bound transition plans aligned with European Climate Law pathways. Replace vague pledges with quantifiable milestones, capex alignment, and governance accountability.

CSRD won’t end marketing. It will end unverified marketing. Build your systems now—so when auditors, buyers, and analysts ask “Can you prove it?”, your answer is a confident yes.

Next step: Grab our Double Materiality Workshop Kit and ESRS Evidence Checklist to operationalize this today.